Nuremberg, March 30, 2021 – The Iran war and the escalating tensions in the Middle East are now clearly impacting the Tour Operator business. In the first two weeks of March, new bookings in Germany dropped sharply (CW 11 & 12: -16 to 20 percent), while demand is increasingly shifting towards western destinations. Bookings for the United Arab Emirates have collapsed, and traditionally strong destinations such as Turkey and Egypt are also experiencing noticeable declines. At the end of February 2026, seasonal figures still reflected solid growth. However, the winter season’s cumulative increase of 4 percent is now under pressure. High cancellation rates for March and April are expected to erode this gain. At the same time, travellers seeking alternatives face rising holiday prices, limiting the potential for replacement bookings.

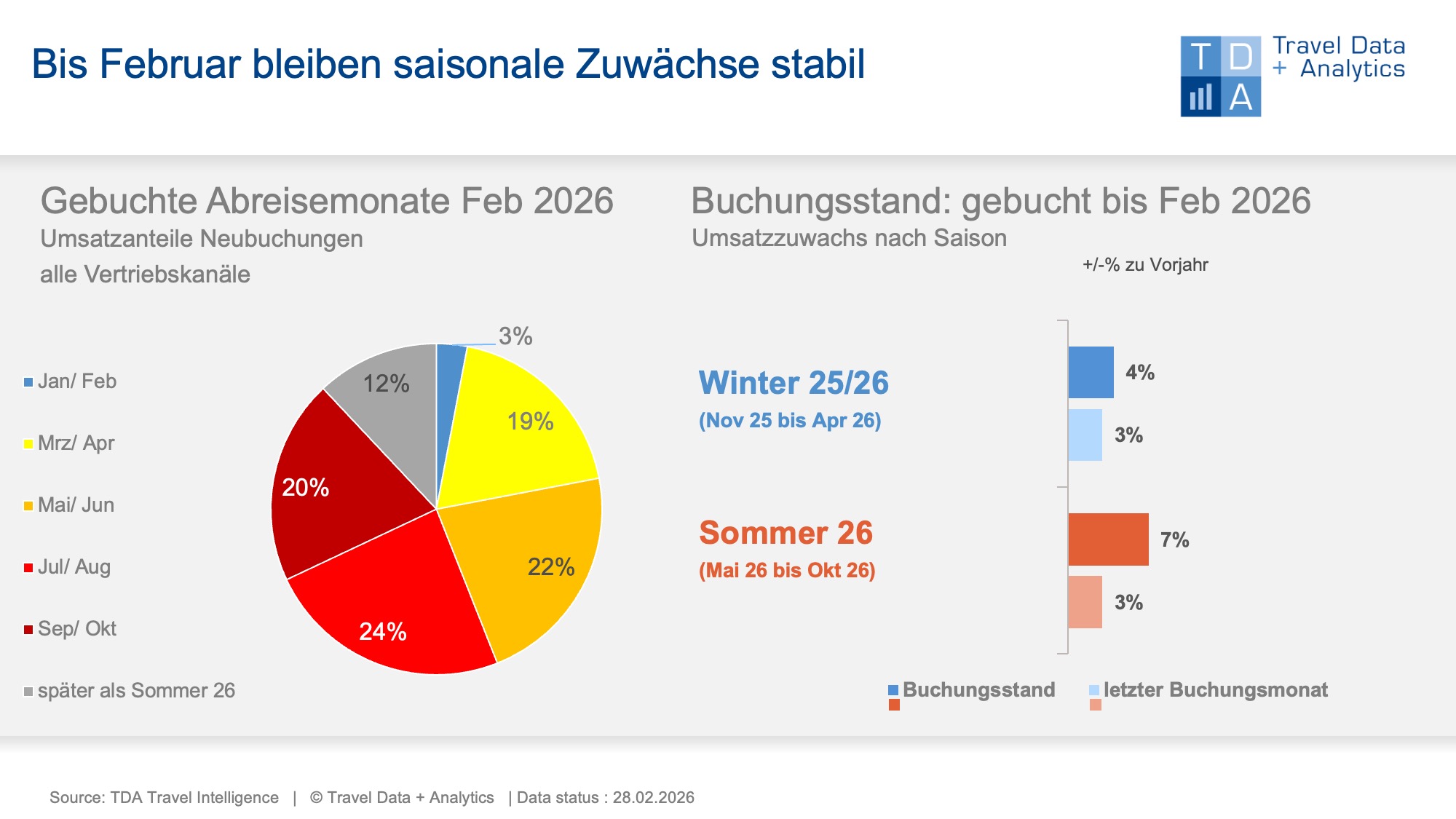

The conflict with Iran began on 28 February 2026, the final day of the month. As a result, the February booking period remains entirely unaffected by the war and escalation in the Middle East – making it an ideal benchmark for assessing and contextualising the market impact that has unfolded since March. As of the end of February, both the ongoing winter season and the upcoming summer season maintained their previous month’s cumulative revenue growth of +4 percent and +7 percent respectively. For the winter season 2025/26, 98 percent of last year’s total winter revenues had already been booked (previous month: 90 percent), although only 63 percent of these trips have actually taken place so far. The travel months of March and April, centred around the Easter holidays, carry significant weight. Given the expected surge in cancellations – particularly for destinations in the Gulf region – combined with the currently observed decline in new bookings, the Middle East conflict is set to have a tangible impact on the final outcome of the winter season.

Early March booking data already points to a clear shift in travel flows: instead of the United Arab Emirates and neighbouring destinations, travellers are increasingly opting for western destinations such as the Canary Islands and the Balearics. Overall, bookings to the eastern mid-haul region have declined by around 10 percentage points. Egypt and Turkey – and with them several regionally strong tour operators – are also affected by the downturn.

“The Middle East conflict poses tangible risks for the holiday travel market,” says Roland Gassner, Director Business Development at Travel Data + Analytics (TDA). “Beyond the direct regional impact, rising energy costs are already pushing up holiday prices – sometimes significantly. Higher travel prices weigh on demand, particularly as household budgets are simultaneously squeezed by increasing fuel and energy costs. If the current situation persists, upward pressure on inflation cannot be ruled out. However, for the time being – especially with regard to the summer season – we expect a redistribution of travel flows and shifts in the market relevance of certain tour operators, rather than a decline in overall travel demand.”

Legend:

The chart illustrates the cumulative travel revenues generated up to the end of February 2026 for the current winter season 2025/26 and the upcoming summer season 2026, each compared with the previous year. TDA’s analysis includes holiday travel bookings made through brick-and-mortar travel agencies as well as online bookings via tour operator platforms and Online Travel Agencies (OTAs), with a focus on package holidays.On the left side of the chart, the percentage share of February 2026 booking revenues allocated to the individual travel months or travel seasons is shown.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03