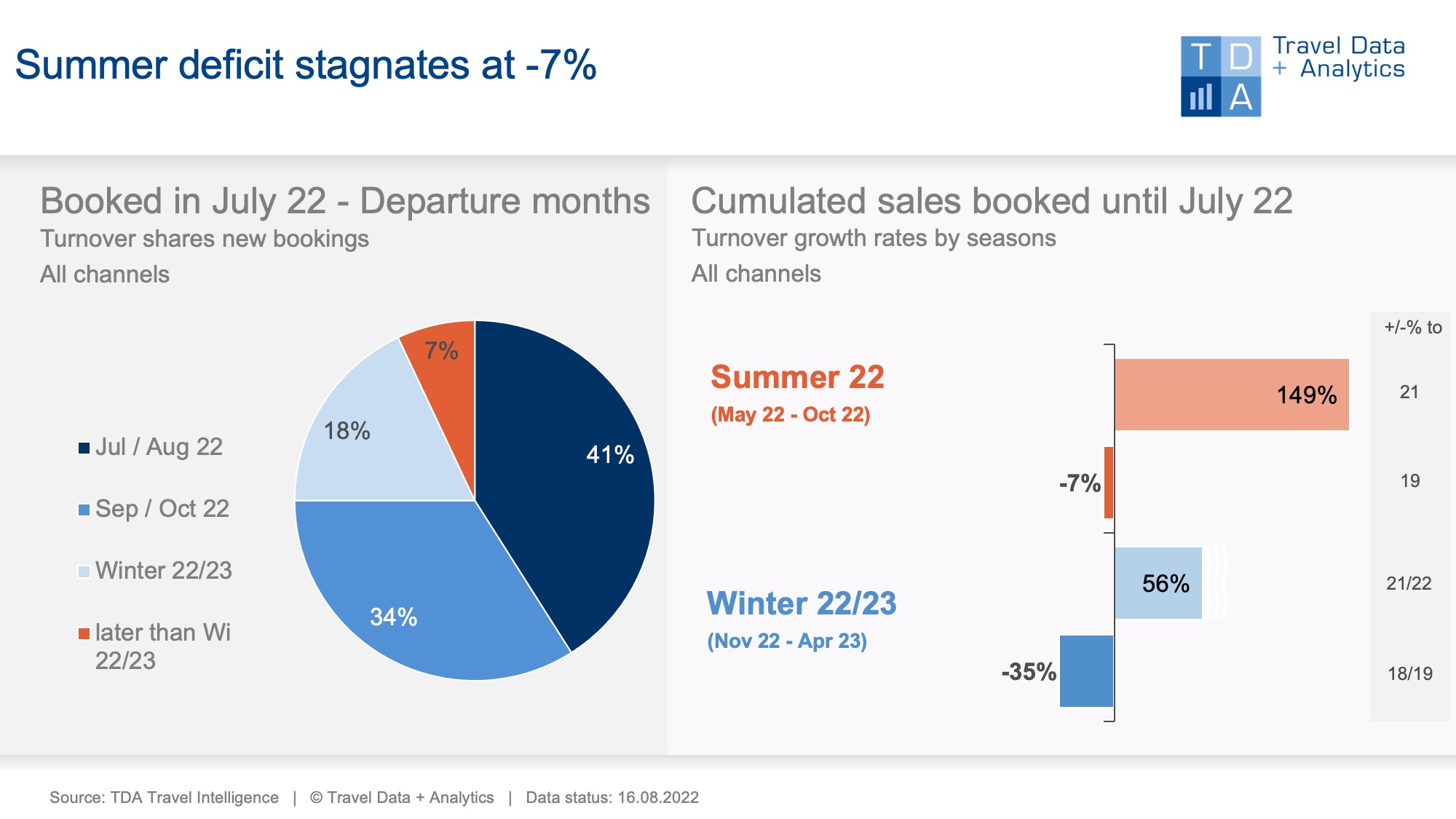

Nuremberg, August 31, 2022 – Short-term holiday travel bookings for the main holiday season in July and August dominate the travel sales business in the booking month of July 2022. Bookings are also increasing for the autumn holidays. Overall, the number of bookings in July has come back to pre-corona levels in 2019. At the current level of bookings, the summer balance thus remains at the level of the previous month (-7 percent). A first look at the upcoming winter season 2022/23 shows: In comparison to 2018/19 (the last winter season unaffected by Corona) bookings are still 35 percent behind.

In July 2022, Germans booked holiday trips for around 1.2 billion euros. Although the number of bookings can no longer keep up with the previous month (-27 percent), it remains at a good level comparable to 2019. With 41 percent of the monthly booking revenue for departures in July/August, the proportion of short-term holiday travel bookings will remain exceptionally high in July 2022. For the autumn months of September and October, bookings are now notably increasing: A revenue share of 34 percent corresponds to an increase of nine percentage points compared to the previous month.

Travel bookings for the upcoming winter season 2022/23 are also slowly increasing, but the advance booking volume achieved so far is only below average overall: Compared to the 2018/19 winter season, the cumulative turnover already booked for holiday travel in the coming winter half-year is still down 35 percent. The previous year's season 2021/22 is significantly exceeded by the current booking level, but a year ago the spreading delta variant and increasing travel restrictions prevented longer-term holiday planning.

Cruises and long-distance travel – both early-booking holiday segments – currently account for well over half of the winter sales achieved so far. The Canary Islands, always the top destination for German holidaymakers in winter, currently account for 26 percent of the tour operator trips in terms of turnover. In order of their sales importance, the most popular winter destinations are Egypt, the Maldives, Dominican Republic, Thailand and Turkey. At the current level of bookings, however, only the Maldives (+1 percent) and Turkey (+10 percent) have succeeded in building on their old strength. At the present time, all other travel destinations still have double-digit percentage arrears compared to the pre-Corona level.

Legend:

The chart shows the cumulative travel sales generated up to the end of July 2022 for the 2022 summer season and the coming 2022/23 winter season in comparison to previous years (2019 and 2021 summer and 2018/19 and 2020/21 winter seasons). For the travel seasons, TDA compares the booking status adjusted for trips that were cancelled in previous years due to corona. Both holiday travel bookings in high street travel agencies and online on the travel portals of the tour operators and online travel agencies (OTAs) with a focus on package tours are included. The chart on the left shows the percentage of sales in the booking month March that is attributable to the individual travel months or seasons.

About TDA Travel Intelligence

Travel Data + Analytics (TDA) took over in spring 2019 the travel sales panel run by the Nuremberg market research company GfK since 2004. After the GfK data had been migrated to a new IT landscape, Travel Intelligence was set up as an independent solution with a self-learning database and associated analysis tool. The basis remains the booking data from stationary travel agencies and online portals that sell tour operator products. The requirements of tourism companies on a modern control instrument and evolving, increasingly dynamic questions can thus be mapped reliably and promptly, without giving up the core of a market-representative method that is consistently comparable over time. TDA = Current booking situation + individual product performance + new market opportunities.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03