Nuremberg, March 28, 2024 – The volume of new bookings in the German holiday market for tour operator holidays remains at a high level, exceeding that of the previous year. Overall, sales generated in travel sales in the booking month of February 2024 were 17 per cent higher than in the same month last year. In terms of cumulative sales, the current 2023/24 winter season exceeded both the final winter results of the 2022/23 season and the 2018/19 season as at the end of February. The remaining two months of bookings will only influence the level of growth in the final result.

With the good level of bookings in the German holiday travel market, sales growth continues to increase compared to pre-crisis levels: The current 2023/24 winter season has improved by two percentage points to a plus of 15 per cent, while the upcoming 2024 summer season has gained four percentage points to a plus of 15 per cent. At the same time, the high growth rates compared to the previous year, which still lacked many early bookers, continue to decline as expected.

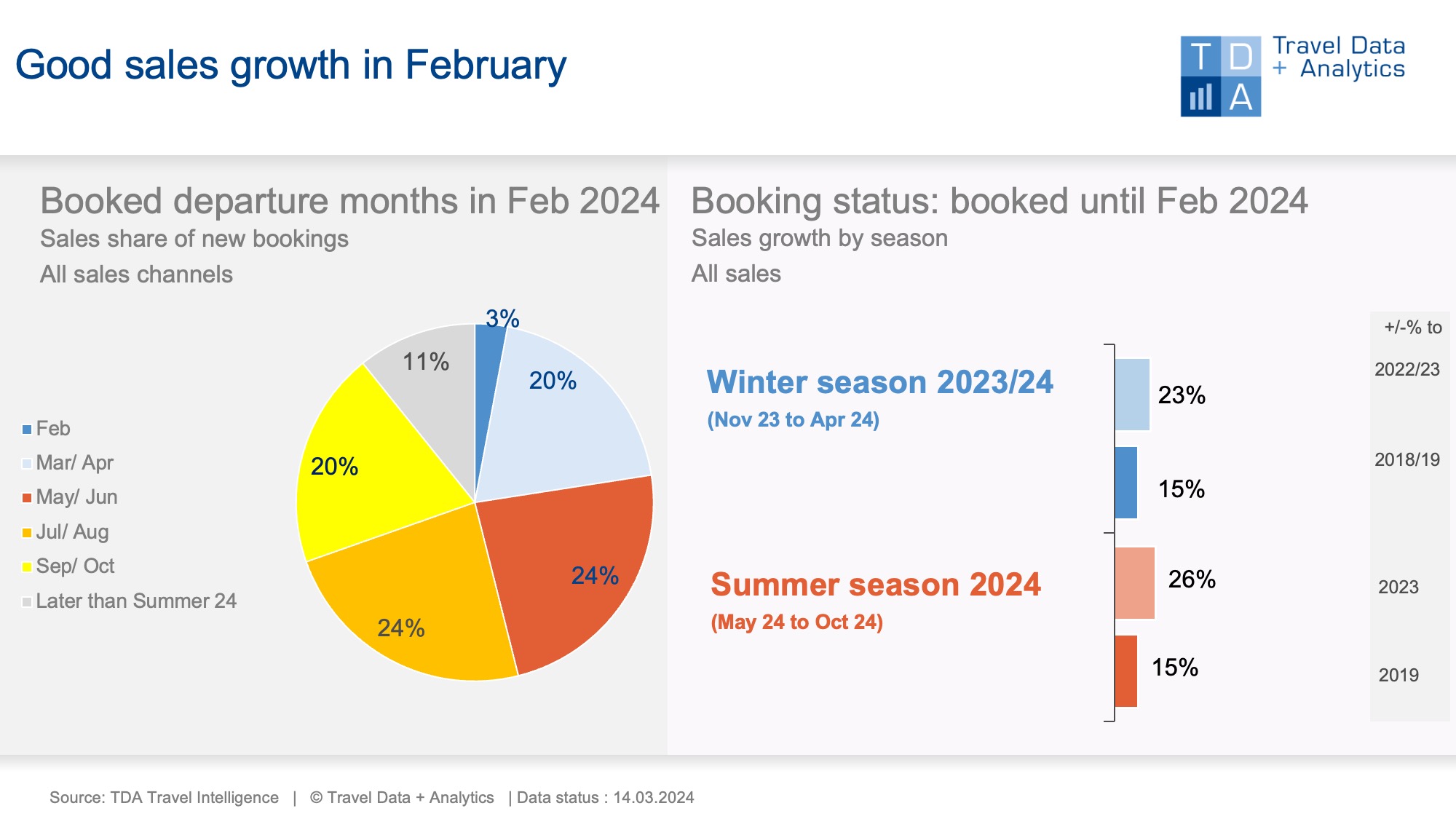

The strong demand for Easter holidays, which were also booked at short notice in February, brings the current winter season cumulative sales of more than 6 billion euros. This means that at the current stage - two months before the end of the season - it has already surpassed the turnover of previous winter seasons (+13 per cent compared to the previous year, +9 per cent compared to winter 2018/19). Only in terms of people booked is it still 10 per cent short of the pre-corona level (previous year: +21 per cent).

Whitsun holidays in May are also heavily booked: no other travel month recorded higher sales in February. Overall, 48% of monthly turnover is attributable to the summer months of May to August, with a further 20% coming from autumn holidays in September and October. Around one in ten holiday euros is also spent on later travel dates from the 2024/25 winter season onwards. The proportion of early bookers has therefore increased by four percentage points compared to both the same month last year and February 2019.

A winter season 2023/24 that is certain to see sales growth and a flourishing summer business in 2024 add up to a promising outlook for the entire 2023/24 tourism year: based on the previous year's total sales, 70 per cent of these had already been achieved by the end of February. To date, the number of guests booked for organised tour operator trips is still 12% below the previous level, but the gap is narrowing from month to month. It cannot be ruled out that this gap can also be closed in the remaining eight booking months.

Legend:

The chart shows the cumulative travel sales generated up to the end of February 2024 for the current winter season 2023/24 and the upcoming summer season 2024 in comparison to the previous seasons and the pre-corona level (summer 2019, winter 2018/19). TDA's analyses include both holiday bookings in brick-and-mortar travel agencies and online on the travel portals of tour operators and online travel agencies (OTAs) with a focus on package holidays. The chart on the left shows the percentage of sales in the booking month of February accounted for by the individual travel months and seasons.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03