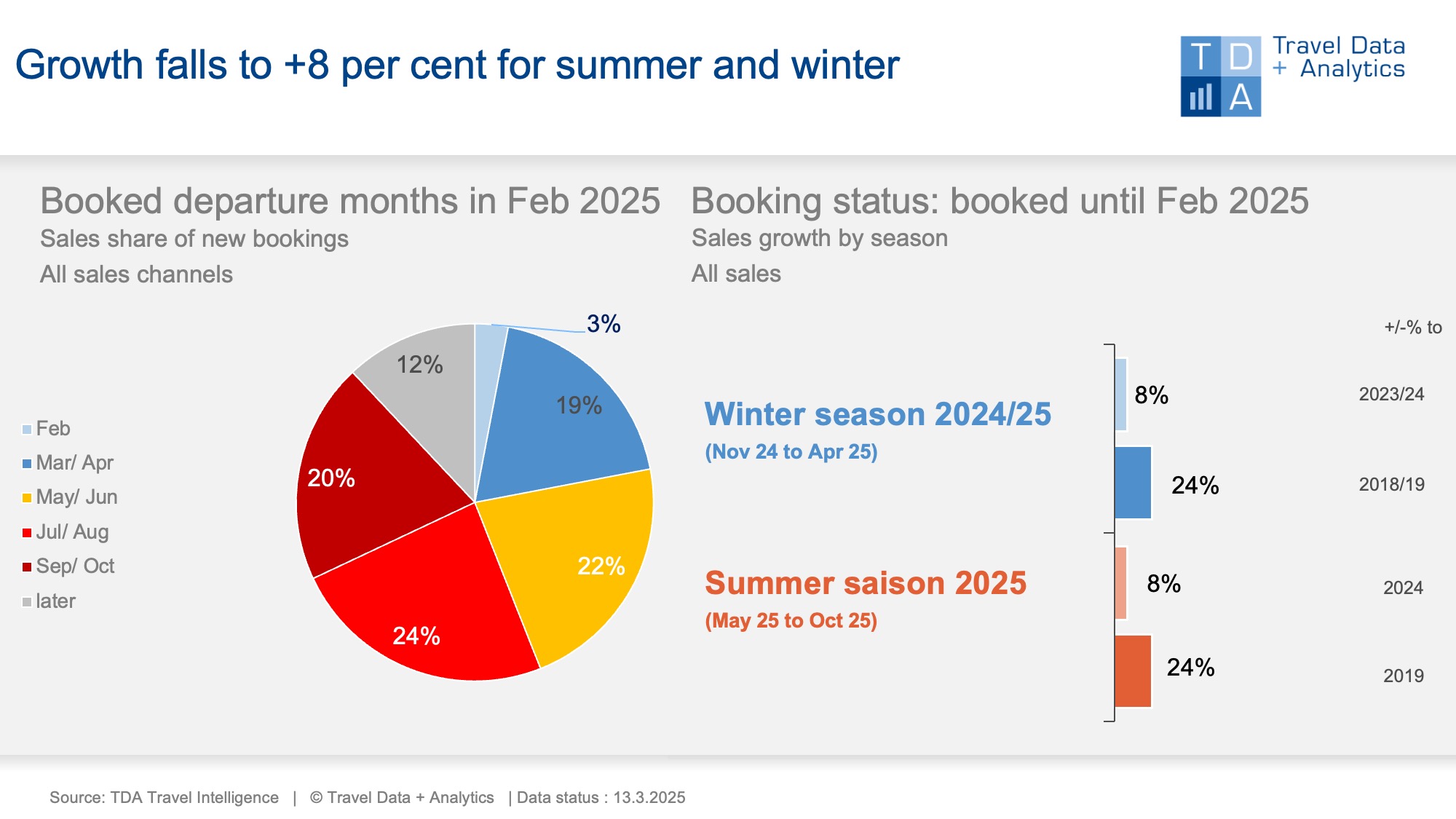

Nuremberg, March 28, 2025 – In the past month of February 2025, booking sales slipped below the previous year's level. With a drop of 11 per cent for the current winter season and minus 9 per cent for the upcoming summer season, the cumulative seasonal growth rates have fallen to single-digit percentages. The 2024/25 winter season loses two percentage points compared to the previous month and now shows an increase in sales of 8 per cent. Overall, however, winter sales are already exceeding the final figure for the previous year's season. Winter growth is certain. The 2025 summer season lost a full four percentage points compared to the previous month and now also stands at a cumulative +8 per cent.

The current winter season 2024/25 has already made it to the current booking status at the end of February: winter sales achieved to date now exceed those of the previous year's season by 1 per cent overall. The remaining two booking and travel months can therefore only boost the final result, even if monthly incoming bookings remain below the previous year's level. At 22 per cent, around a fifth of the monthly turnover in February is still due to winter holidays. Almost half of this goes to the Easter holidays in April.

The past booking month of February also heralds the end of double-digit growth rates for the upcoming 2025 summer season. The development was foreseeable: after all, incoming bookings are again running against a good previous year. With a cumulative increase in turnover of currently 8 per cent, the summer season has now reached 52 per cent of the total turnover of last year's summer (previous month: 43 per cent). In terms of people booked - not turnover - 46 per cent of holidaymakers are attracted to countries in the eastern medium-haul region for their summer holidays, particularly Turkey, Greece and Egypt. Around one in four people travel to holiday destinations in western Europe, preferably to the Balearic or Canary Islands, Italy, Portugal or holiday regions on the Spanish mainland. Overall, the number of people booking package holidays or holidays organised as building blocks fell almost to the previous year's level (+1 percent) due to the weaker February volume. Early bookers, who are already securing their holidays for next winter or even later, increased significantly to 12% of monthly sales in February. In the previous month, this figure was only 7 per cent.

Legend:

The chart shows the cumulative holiday bookings generated by the end of February 2025 for the current winter season 2024/2025 and the upcoming summer season 2025 compared to the previous year and the pre-corona level (summer 2019, winter 2018/19). TDA's analyses include holiday travel bookings in brick-and-mortar travel agencies as well as online on the travel portals of tour operators and online travel agencies (OTAs) with a focus on package holidays. The chart on the left shows the percentage of sales in the booking month of January accounted for by the individual travel months and seasons.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03