Nuremberg, November 28, 2024 – German citizens spent around 15 billion euros on their summer holidays organized by tour operators this year - a new record. This means that the 2024 summer season ends with a year-on-year increase in turnover of 10 per cent as at the end of October 2024. The tourism year as a whole, including the previous winter season 2023/2024, closed with an increase of 12 per cent. At the start of the new winter 2024/2025 travel season on 1 November, 60% of the previous winter season's sales had already been booked - a good starting position that remains unchanged. However, the volume of early bookings for summer holidays next year is outstanding.

Like the previous winter season 2023/24, the 2024 summer season, which has now ended, shows very good results, with sales up by 10 per cent. The number of people booked a tour operator trips is also up 3 per cent on the previous year. However, they are not yet keeping pace with the pre-corona level in summer 2019: they are 9 per cent lower - while holiday sales are 24 per cent higher than in the 2019 summer season. There are several reasons for the gap between sales and the number of guests booked: Price increases play a role, as does the return of more expensive forms of holiday such as long-haul travel and the generally positive spending behaviour when it comes to holidays. The year-on-year growth underlines the high value that holidays enjoy in this country. However, the decline in the number of people booking holidays also indicates that there are still households that have to cut back on holidays in view of the rising cost of living. Another trend that is consolidating: More and more holidaymakers are tending to book online. In terms of revenue, 40 per cent of this year's summer holidays in 2024 were booked on traditional travel portals - with above-average growth of 19 per cent compared to the previous summer. In summer 2019, the online share was only 33 per cent, accounting for less than half of the sales volume.

The past 2024 summer season contributed 70 percent of total sales in the holiday business for package tours and modular tours to the overall pleasing annual result. Including the previous winter season 2023/24, which closed with a 20 per cent increase in turnover, the tourism year now ended achieved 12 per cent growth compared to the previous year (bookings: +8 per cent).

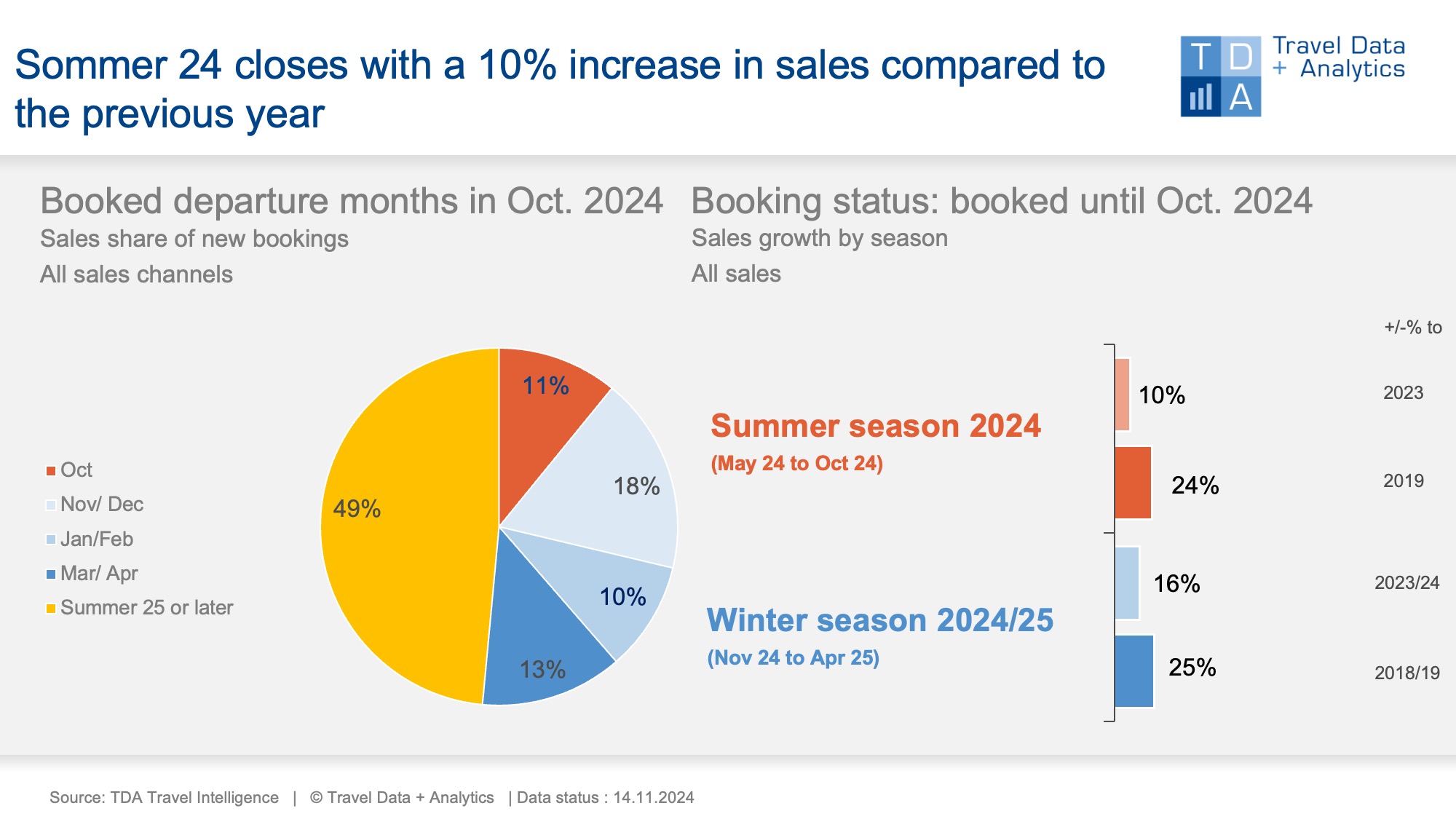

Early bookers for the 2025 summer season are showing particularly strong growth: in the booking month of October, almost every second holiday euro in travel sales is already owed to summer holidays for the coming year. This means that early bookers are gaining 5 percentage points in terms of sales compared to the same month last year. The fact that holidaymakers are already focusing so strongly on summer 2025 is to some extent at the expense of the 2024/25 winter season, which began with the travel month of November. 41 per cent of monthly sales in October were attributable to upcoming winter holidays, 2 percentage points less than a year ago and 9 percentage points less than in pre-crisis times in October 2019. However, the current winter season had already benefited from strong early bookings and is feeding off this. Accumulated sales for winter 2024/25 are currently still up 16 per cent on the previous year. Compared to the previous month, the lead has shrunk by two percentage points.

Legend:

The chart shows the cumulative travel sales generated up to the end of October 2024 for the current winter season 2023/24 and the upcoming summer season 2024 in comparison to the previous seasons and the pre-corona level (summer 2019, winter 2018/19). TDA's analyses include both holiday bookings in traditional travel agencies and online on the travel portals of tour operators and online travel agencies (OTAs) with a focus on package holidays. The chart on the left shows the percentage of sales in the booking month of April accounted for by the individual travel months and seasons.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03