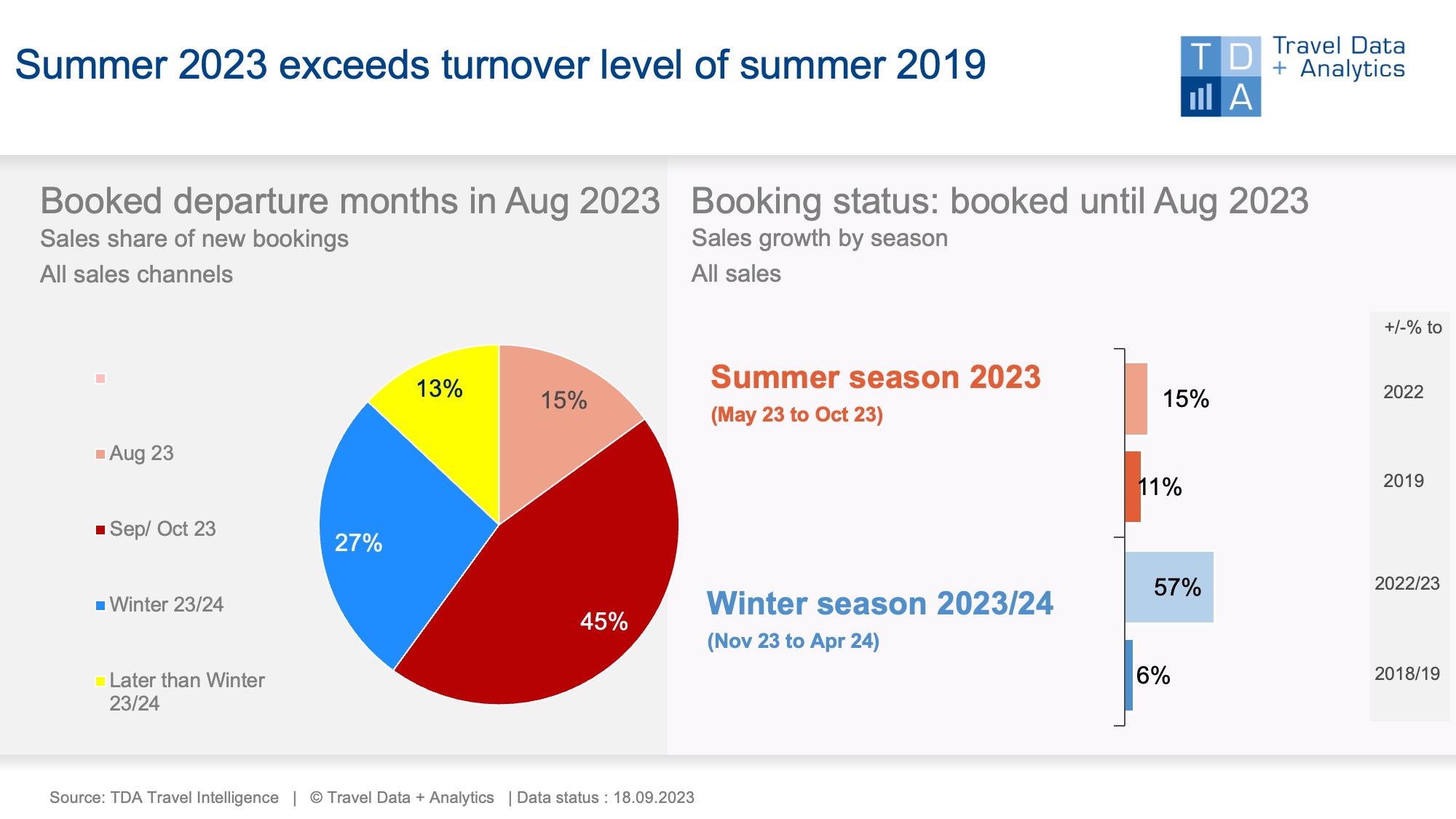

Nuremberg, 29 September 2023 - In the latest month of reporting, the current 2023 summer season had already exceeded the final result of the previous year's summer. Now it is well done so in comparison to the pre-Corona level of summer 2019: As of the booking status at the end of August 2023 - two months before the end of the season - the increase in sales amounts to 6 per cent on the final level of the summer season 2019 and 8 per cent on the final level of the previous year's summer. The Germans' desire to go on holiday remains high. Booking turnover in travel agencies and on the classic travel portals of tour operators and OTAs in August far exceeds both the same month last year (+23 per cent) and August 2019 (+32 per cent).

The holiday business is definitely back on track after the Corona pandemic: For the still ongoing summer season, a strong shift to the Eastern Mediterranean travel destinations can be observed (+36 per cent) and especially earthbound travel and long-haul travel have not yet been able to regain their former strength. For the upcoming winter season 2023/24, however, long-haul travel is approaching its previous sales level again and cruises have already surpassed the pre-Corona level. However, a significant share of the good sales development in the holiday travel business is due to higher prices and holiday spending as a result of inflation. In terms of booked people, the 2023 summer season is 14 per cent short of the current booking level, the coming winter season 17 per cent. There is still a gap between sales growth and the number of people booked. In other words, not all households in Germany seem to be able to afford an organised tour operator trip this year in view of the increased cost of living. However, it is also true that 7 per cent more people have already travelled on an organised tour operator trip during the summer holidays than last year.

In August 2023, booking behaviour is still more short-term oriented than it used to be: 15 per cent of monthly turnover is due to last-minute holiday bookings departing in August. Another 45 percent are accounted for by holiday bookings for the autumn months of September and October. Winter holidays are below average in terms of turnover at 27 per cent: Around 6 percentage points are missing compared to August 2019.

Cumulatively, the new winter season 2023/24 shows an increase in turnover of 57 percent compared to the previous year at the current booking level at the end of August. There is no sign of any booking restraint this year as there was last year. In terms of tour operator travel (excluding cruises), the Canary Islands remain by far the top winter destination - followed by Egypt with strong growth. Together, these two holiday destinations account for 45 per cent of winter sales to date. Turkey, which is clearly gaining in importance as a winter destination, is also showing particularly strong growth.

Legend:

The chart shows the cumulative travel sales generated up to the end of August 2023 for the ongoing summer season 2023 in comparison to previous years (summer season 2019). For the travel seasons, TDA compares the booking status adjusted for trips that were cancelled in previous years due to corona. Both holiday travel bookings in high street travel agencies and online on the travel portals of the tour operators and online travel agencies (OTAs) with a focus on package tours are included. The chart on the left shows the percentage of sales in the booking month October that belongs to the individual travel months or seasons.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03