Nuremberg, April 29, 2026 – Bookings of leisure trips for the current winter season plummeted by nearly half in March, and by just under a fifth for the upcoming summer season. Taken together, the decline in bookings over the past booking month amounts to a total of 25 percent for the current 2025/26 tourism year. These steep losses indicate that the high volume of cancellations for destinations in the Middle East could not be offset by rebookings by a long shot. Even more concerning is the pronounced reluctance to book that emerged in March. The losses caused by the war in Iran are costing growth in the German vacation travel market: The winter season has lost a cumulative 2 percentage points compared to the previous month, while the summer season has dropped by as much as 4 percentage points. Nevertheless, both seasonal balances remain positive.

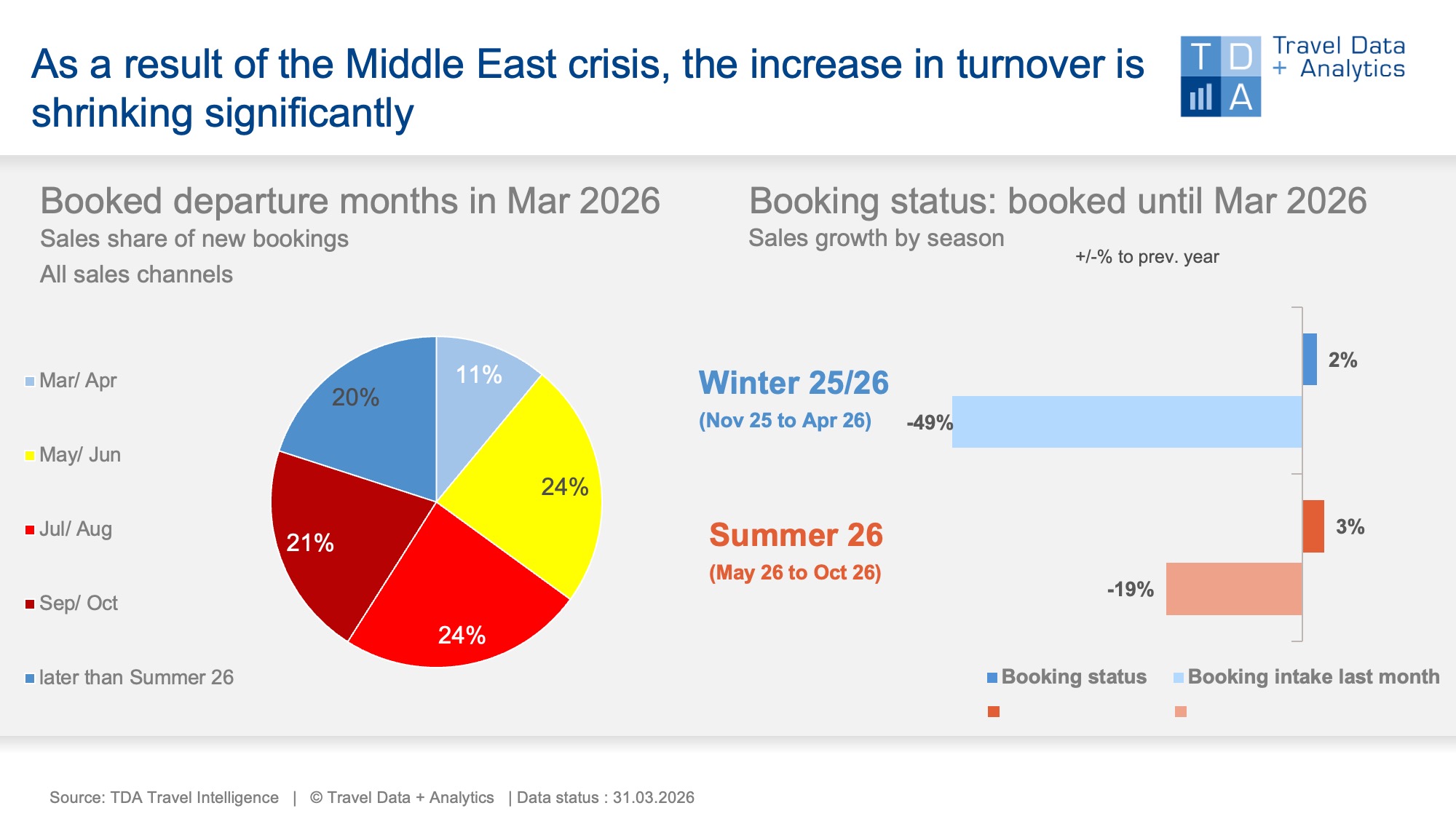

Although cancellations, rebookings, and new bookings for the winter season—which runs through the end of April—totaled a 49 percent decline in March, the overall winter performance remains positive at 2 percent. And as small as the revenue volume may have been—it was sufficient for the winter season, based on current bookings, to match the final seasonal revenue of the entire previous winter (occupancy: 100 percent). However, not all vacations with departures to the Emirates in April have been canceled yet, nor have long-haul trips via their major hubs been rebooked, and the volume of new winter bookings remains well below last year’s level even in the first weeks of April. The current winter surplus is fragile.

For the upcoming summer season, the first signs of relief are emerging in the calendar week following the Easter holidays (Calendar Week 16): vacation bookings are picking up again. By the end of March 2026, however, the summer season has lost 4 percentage points of its previous growth and has fallen back to a cumulative revenue increase of 3 percent. The occupancy rate reached as of the end of March, currently at 59 percent, is slightly lower than last year (61 percent).

Gulf states, neighboring vacation destinations, and long-haul travel with the sharpest declines

It comes as no surprise that travel destinations in the Gulf region have suffered immense losses in March due to existing travel advisories and cancellations by tour operators. In the United Arab Emirates alone, more than a quarter of winter revenue has already had to be written off. Due to restricted air travel, long-haul destinations such as the Maldives or Thailand, as well as neighboring vacation destinations like Turkey and Egypt, are also being hit hard by a drop in bookings. Before the outbreak of the Iran war, Turkey was the most-booked destination for the coming summer, with above-average growth of 12 percent compared to the previous year. Following the losses in March (-46 percent), the revenue increase has shrunk to 3 percent, and Turkey has slipped to second place in the summer rankings. For Egypt, the previously accumulated summer growth of 15 percent has fallen to 1 percent after just one month.

Overall, Eastern Europe’s medium-haul market lost 34 percent in March compared to the same month last year. Greece got off relatively lightly with a 10 percent drop in bookings and is once again among the most-booked summer destinations in April. Otherwise, vacationers are preferring western destinations. Spanish vacation regions are benefiting in particular: Mainland Spain saw a 32 percent increase, while the Canary Islands and the Balearic Islands each saw a 15 percent increase. Italy (+8 percent) and Portugal (+3 percent) are also bucking the negative March trend, which has affected all other travel regions—as well as cruises (-18 percent)—with the exception of Western Europe (medium-haul) (+16 percent) and land-based travel (+2 percent).

Legend:

The chart shows the cumulative travel revenue generated through the end of March 2026 for the current 2025/26 winter season and the upcoming 2026 summer season, each compared to the previous year. TDA’s analyses include both vacation bookings made at brick-and-mortar travel agencies and online bookings on tour operators’ travel portals and Online Travel Agencies (OTAs), with a focus on package tours. The left side of the chart shows the percentage of revenue in the booking month of March 2026 attributable to the individual travel months or seasons.

About TDA Travel Intelligence

Travel Data + Analytics GmbH (TDA) is a data analytics and business intelligence provider for the tourism industry. With Travel Intelligence, TDA operates a data-driven analytics platform for tourism sales. The platform is based on continuously collected booking data from high street travel agencies as well as online sales channels for tour operator products. Data is processed using a modern system architecture that employs advanced analytical techniques and AI-driven methods. The solution supports tourism companies in assessing current booking trends and identifying market potential.

TDA stands for: current market volume + individual market shares + realizable growth potential.

Further information: Alexandra Weigand, alexandra.weigand@traveldataanalytics.de, phone: +49 (0)911 951 510 03